23rd Apr, 2026| 5 Min read.

How to calculate Goodwill value while acquaring a business?

Goodwill valuation process

When acquiring a business, goodwill is basically the extra amount you pay above the fair value of its identifiable assets. It reflects things like brand reputation, customer loyalty, and future earning potential.

Core idea

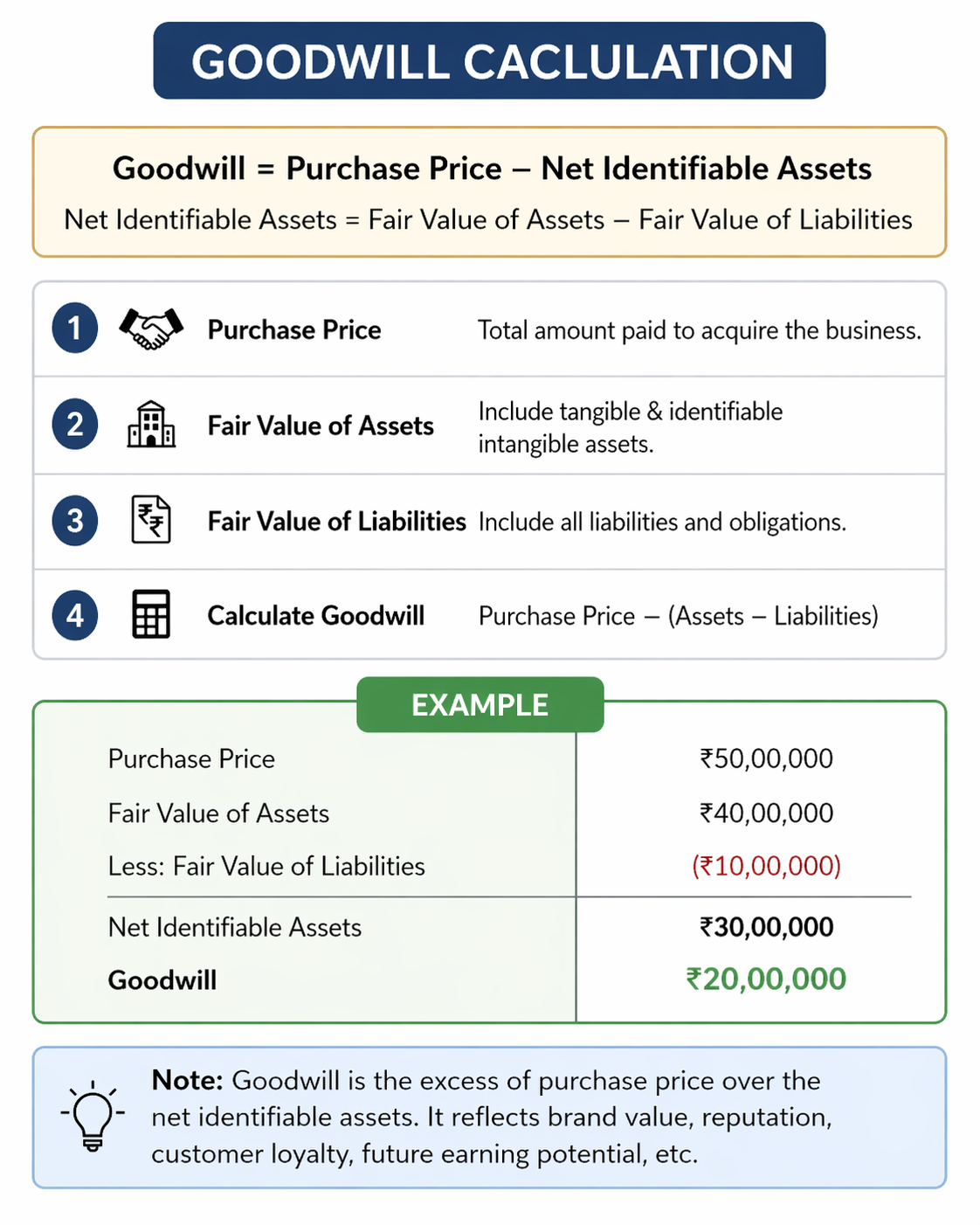

Goodwill = Purchase Price – Net Identifiable Assets

Here’s the formula clearly:

Step-by-step method

1. Determine Purchase Price

This is the total amount you pay to acquire the business (cash, shares, etc.).

2. Find Fair Value of Assets

Include:

- Tangible assets (land, machinery, inventory)

- Identifiable intangible assets (patents, trademarks)

3. Subtract Liabilities

Include:

- Loans

- Payables

- Any obligations

Net Identifiable Assets = Assets – Liabilities

4. Calculate Goodwill

Subtract net assets from purchase price.

Example

Suppose:

- Purchase price = ₹50 lakh

- Fair value of assets = ₹40 lakh

- Liabilities = ₹10 lakh

Net assets = ₹40L – ₹10L = ₹30L

Goodwill = ₹50L – ₹30L = ₹20 lakh

That ₹20 lakh is goodwill.

Alternative methods (used in valuation)

Sometimes goodwill is estimated before acquisition using:

1. Average Profit Method

Goodwill = Average Profit × Number of Years Purchase

2. Super Profit Method

Goodwill = Super Profit × Years Purchase

- Super Profit = Actual Profit – Normal Profit

3. Capitalization Method

Based on expected return on investment.